Unraveling the Mysteries Behind Credit Cards- Look Past 0% Offers

Unraveling the Mysteries Behind Credit Cards- Look Past 0% Offers

Hey there, my fellow credit enthusiasts!

Ready to dive into the world of credit cards and decode those tricky terms and conditions?

Before you take the plunge into the enticing ocean of sign-up bonuses and 0% offers, let me, your Credit Queen, equip you with the ultimate guide of knowledge and wisdom necessary to navigate the complex world of credit cards and to avoid those dreaded surprises down the line.

The Comprehensive Guide to Credit Card Terms and Conditions

In this comprehensive guide, we will delve into the nitty-gritty details of credit card terms and conditions, uncovering their meanings and highlighting key things to look out for. So, grab your crown and let’s begin our journey!

First Rule of the Credit Card Club: Know Thy Terms and Conditions

Hold up, before you go on a credit card shopping spree, pause and ponder.

Have you done your homework, studying the fine print of that dazzling offer?

Don’t let the promise of endless beach vacations lead you astray– Those terms and conditions aren’t just there for decoration. They’re like the map to the hidden treasures (or pitfalls) you might face.

The Sneaky World of Terms and Conditions

Ever heard of the credit card version of a fairy tale? It’s called “Terms and Conditions.”

This magical manuscript is where credit card companies reveal their hidden secrets.

Did you know that once you swipe that card, it’s like a magical contract you’re locked into with the card issuer?

But fear not, I’ll show you the key to unlocking those mysteries.

What are Credit Card Terms and Conditions?

Credit card terms and conditions are the formal statements that outline the rules and guidelines governing the relationship between a credit card issuer and a cardholder1.

They serve as a legally binding agreement, detailing important information such as fees, interest rates, penalties, balance transfer terms, and cash rewards2.

Familiarizing yourself with these terms and conditions is crucial for responsible card usage and can help you avoid unnecessary fees and penalties3.

Where to Find Your Goldmine: Hunt Down Those Sneaky T&C’s!

Ready to embark on a treasure hunt?

Your quest begins with that oh-so-sly “Terms and Conditions” link.

No need to be a Sherlock! Look for that “Terms and Conditions” link near the tempting “Apply” button.

Sometimes it’s a little like finding Waldo, but with a lot more dollars at stake! If that link’s playing hide-and-seek, don’t worry. Search for phrases like “benefits and terms” or “rates and fees” – they’ll guide you to the pot of gold (or caution).

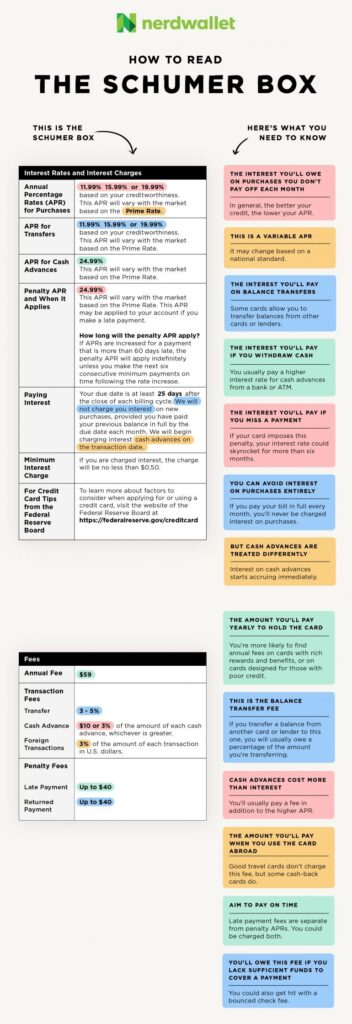

Meet the Schumer Box

Ever wanted to decode financial hieroglyphics? Look no further than the Schumer Box – a treasure trove of numbers and jargon. At the very top, you’ll spot the APR, the magic number that determines your fate.

But wait, there’s more!

Dive into the fine print, where the nitty-gritty of payment allocation, rewards, and benefits await.

The Ultimate Checklist: Navigating Terms and Conditions

Key Terms and Conditions to Know

Now, let’s dive into the key terms and conditions you need to be aware of when it comes to credit cards. Remember, knowledge is power!

1. Annual Percentage Rate (APR)

- The magical number that determines how much borrowing costs you.

- Look out for: Introductory rates that skyrocket after a few months.

The annual percentage rate is the interest rate charged on any outstanding balances on your credit card3. It is important to pay attention to the APR, as it can significantly impact the cost of borrowing.

Here are some key things to look out for:

- Introductory APR: That 0% promise? Uncover its secrets: watch for traps, transfer fees, and the dreaded deferred interest curse! Some credit cards offer a lower introductory APR for a certain period of time. Be aware of when this introductory period ends and what the APR will be afterwards.

- The golden ticket to low initial interest rates.

- Look out for: How long the intro period lasts and the APR that follows.

- Variable APR: Some credit cards have a variable APR, which means it can fluctuate based on market conditions. Understand how the APR can change and what factors may influence it.

- The sneaky rate that can change with the economic winds.

- Look out for: Understanding how the rate is calculated and potential hikes.

- Penalty APR: If you miss a payment or violate the terms of your credit card agreement, the issuer may impose a penalty APR, which is a higher interest rate. Be aware of the conditions that may trigger a penalty APR and the steps you can take to avoid it.

- Late Payment Fee:

- The price of forgetting your royal duties.

- Look out for: Grace periods and the maximum fee you can be charged.

- Overlimit Fee:

- The punishment for exceeding your credit limit.

- Look out for: Opting out of over-limit fees to avoid unnecessary charges.

- Late Payment Fee:

2. Credit Limit

The credit limit is the maximum amount of money you can borrow on your credit card1. It is important to understand your credit limit and manage your spending accordingly. Here are some key things to consider:

- Credit Utilization: Your credit utilization ratio is the percentage of your available credit that you are currently using. It is generally recommended to keep your credit utilization below 30% to maintain a good credit score. Be mindful of your spending to avoid maxing out your credit limit.

- Credit Limit Increases: Some credit card issuers may offer credit limit increases over time. Understand the process for requesting a credit limit increase and the factors that may influence the issuer’s decision.

- The throne of your credit empire, dictating your spending power.

- Look out for: Staying below 30% (as previously mentioned) of your limit to avoid credit score damage.

3. Fees

Welcome to the Fee Circus! Don’t be fooled by the cash advance APR! Hidden fees and cash advance woes await the unwary.

Credit cards often come with various fees that can impact your overall cost of using the card. Here are some common fees to be aware of:

- Annual Fee: Is that membership fee giving you the royal treatment or just draining your wallet? Some credit cards charge an annual fee for the privilege of using the card. Consider whether the benefits and rewards of the card outweigh the annual fee.

- Late Payment Fee: If you fail to make your minimum payment by the due date, the credit card issuer may charge a late payment fee. Be sure to make your payments on time to avoid this fee.

- The price of forgetting your royal duties.

- Look out for: Grace periods and the maximum fee you can be charged.

- Balance Transfer Fee: If you transfer a balance from one credit card to another, the issuer may charge a balance transfer fee. Understand the fee amount and whether it is worth it for your specific situation.

- The toll you pay to move debt from one card to another.

- Look out for: High fees that might outweigh potential savings.

Overlimit Fee:

- The punishment for exceeding your credit limit.

- Look out for: Opting out of over-limit fees to avoid unnecessary charges.

Cash Advance Fee:

- The cost of borrowing cold, hard cash from your card.

- Look out for: High fees and interest rates, plus no grace period.

Foreign Transaction Fee:

Foreign Woes: Ever shopped overseas? Those foreign transaction fees are stealthy beasts, ready to pounce.

- The tax for using your card in foreign lands.

- Look out for: Cards with no foreign transaction fees for frequent travelers.

4. Grace Period

- The time you have to pay your balance before interest kicks in.

- Look out for: How many days you have and if it applies to new purchases.

The grace period is the amount of time you have to pay your credit card bill in full without incurring any interest charges1. Here are some key things to know about the grace period:

- Length of Grace Period: Different credit cards may have different grace periods. Understand how long your grace period is and when it starts and ends.

- Interest on Cash Advances: Be aware that cash advances usually do not have a grace period, and interest charges may start accruing immediately.

5. Minimum Payment:

- The smallest amount you must pay to stay in the king’s good graces.

- Look out for: Paying just the minimum can trap you in a debt cycle.

6. Rewards and Benefits

- The treasure trove of perks for your loyalty.

- Look out for: The fine print on earning and redeeming rewards.

Don’t be a damsel in distress – understand earning rates, caps, and those tricky redemption rules.

Many credit cards offer rewards programs and additional benefits to cardholders. Here are some things to consider:

- Reward Structure: Understand how the rewards program works, including the earning rate, redemption options, and any limitations or restrictions.

- Introductory Offers: Look out for those sign-up bonus surprises! The sirens of credit cards, luring you with bonuses. But beware limits and loopholes before you dive in. Some credit cards may offer introductory bonuses or special rewards for a limited time. Be aware of these offers and any requirements to qualify.

- Additional Benefits: The card’s hidden perks – a magic carpet ride or a wild goose chase? Unearth the truth. Credit cards may come with additional perks such as travel insurance, purchase protection, or access to airport lounges. Familiarize yourself with these benefits and how to take advantage of them.

The Credit Card Act of 2009 and the Truth in Lending Act

Before we conclude our journey through the world of credit card terms and conditions, it is important to mention two key pieces of legislation that protect consumers: the Credit Card Act of 2009 and the Truth in Lending Act.

The Credit Card Act of 2009 was enacted to enhance consumer protections and promote transparency in credit card agreements. It introduced several important provisions, including:

- Restrictions on Interest Rate Increases: Credit card issuers are limited in their ability to increase interest rates on existing balances.

- Advance Notice of Rate Changes: Issuers must provide at least 45 days’ notice before making significant changes to the terms of a credit card agreement.

- Clearer Disclosure of Terms: Credit card issuers are required to provide clearer and more concise disclosures of terms and conditions, making it easier for consumers to understand their rights and obligations.

The Truth in Lending Act is a federal law that requires lenders to disclose key terms and costs associated with credit products. It ensures that consumers have access to clear and accurate information about the cost of credit, allowing them to make informed decisions.

Conclusion: Empower Yourself with Knowledge

Congratulations, my credit-savvy friends!

You have now journeyed through the intricate world of credit card terms and conditions. Armed with this comprehensive guide, you are equipped to navigate the credit card landscape with confidence and make informed decisions.

Remember to always read the fine print, understand the terms and conditions, and stay vigilant in managing your credit. Now, go forth and conquer the credit world, my fellow Credit Queens and Kings!

Are you ready to take control of your credit?

Join our Credit Queen community today and gain access to exclusive tips, tricks, and resources to help you master the art of credit management. Together, we can build a kingdom of financial success!

*Infographic Source: [Nerd Wallet]

Citations:

[1] https://www.investopedia.com/terms/t/terms-and-conditions-credit-card.asp

[2] https://www.creditkarma.com/credit-cards/i/credit-karma-guide-credit-card-terms-conditions

[3] https://www.nerdwallet.com/ca/credit-cards/credit-card-terms-and-conditions

[4] https://www.wellsfargo.com/credit-cards/agreements/

[5] https://www.consumerfinance.gov/credit-cards/agreements/

[6] https://www.creditcards.com/credit-management/how-to-read-credit-card-terms-and-conditions/

Your articles are extremely helpful to me. Please provide more information!

You helped me a lot with this post. I love the subject and I hope you continue to write excellent articles like this.

I enjoyed reading your piece and it provided me with a lot of value.

I’m so in love with this. You did a great job!!

I want to thank you for your assistance and this post. It’s been great.