Let’s talk about compound interest and how it can either make you rich or drown you in debt. Brace yourself, it’s about to get interesting!

Compound interest is all about the magic of interest building on top of interest. So, when you’re saving or investing, it’s like a snowball effect, and your money grows faster. But if you’re borrowing money, sorry to break it to you, but you’ll end up paying interest on top of interest. Ouch!

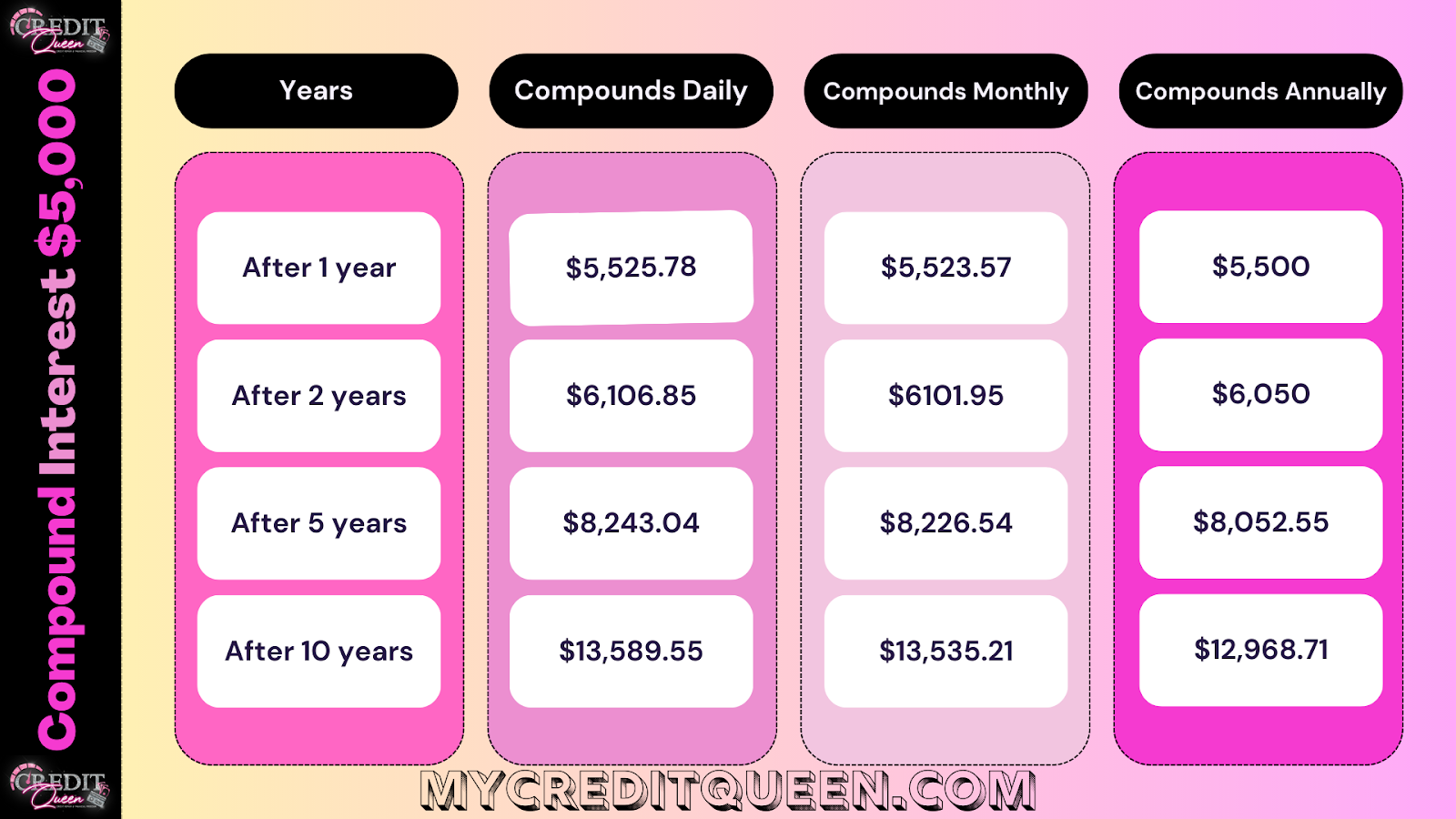

Now, let’s break it down with an example, shall we?

Imagine: you put $5,000 into a savings account with a 10% interest rate that compounds annually. After the first year, you’ll have $5,500. Cha-ching! That extra $500 is the interest you earned on your original $5,000.

Fast forward to the end of the 10th year, and you’ll be sitting pretty with $12,968.71. That’s more than double your initial savings! Thank you, compound interest.

But wait, there’s more!

Savings accounts often compound interest more frequently than once a year. To make things less complicated, they use something called the annual percentage yield (APY), which already includes compounding. It’s like a one-stop shop for figuring out your potential earnings.

Now, I know you might be thinking, “Do I have to bust out my calculator and solve some complex formula?” Fear not, my friend! There are plenty of online calculators to do the math for you (like the one below). But in case you’re curious, the formula for compound interest is:

A = P(1 + r/n)(nt)

Where:

- A is the total amount you’ll end up with

- P is the starting amount (also known as the principal)

- r is the annual interest rate (written as a decimal)

- n is the number of times the interest compounds each year

- t is the total number of years

Don’t worry, you don’t have to become a rocket scientist. Just plug in your numbers and let the calculators do the heavy lifting.

When it comes to deciding whether to save or borrow, there are two factors to consider: the interest rate and the compounding frequency.

A higher interest rate means more money in the long run, and the more often interest compounds, the faster your money will grow.

For example, let’s say you have $5,000 with a 10% interest rate. If it compounds annually, you’ll have a certain amount at the end of the timeframe. But if it compounds monthly or daily, that amount will skyrocket!

Ready to expose the dirty secrets of compounding interest and credit card debt?

Buckle up, because we’re about to dive into the world of daily interest charges and sneaky compounding schedules.

Let’s say you have a credit card with a $20,000 balance. Seems innocent enough, right? But here’s where it gets interesting. This little piece of plastic has an APR of 29% and a daily periodic rate of 0.29 / 365 = .00079. (Some credit card issuers play by their own rules and use 360 days instead of 365. Sneaky, right?)

So, what happens when you don’t make any new purchases or payments?

Brace yourself for the ride.

- On day one, you have a $20,000 balance. Nothing too exciting yet.

- Day two arrives, and the card issuer starts crunching numbers. They add any new transactions to your previous day’s balance (including accrued interest). Crunch, crunch. The result? Your balance increases to $20,015.80, thanks to $15.80 in interest.

- This cycle repeats itself on day three, day four, and so on. The daily interest amount increases each day, making your balance grow faster than a teenage boy going through a growth spurt.

But here’s the catch: you won’t see those interest charges added to your balance if you’re checking your account daily. Nope, they play hide and seek behind the scenes.

Your turn calculate your compound interest using the calculator below:

Instead, credit card issuers have a magic trick up their sleeves

They take the sum of your daily balances throughout the billing cycle, divide it by the number of days in the cycle, and voila – average daily balance, baby!

They then multiply that by your daily periodic rate and the number of days in the cycle, and tada – more interest charges! Clever, huh?

But here’s the real kicker.

The compounding doesn’t cause a massive leap in interest charges from one day to the next. Sneaky compounding is one reason paying off credit card debt can feel like trying to catch a unicorn.

Beware credit card debt isn’t the only debt that compounds

But credit card debt isn’t the only place you’ll encounter this compounding madness. Other types of loans may compound interest monthly or even annually. But fear not, my friend, for there are:

Ways to avoid being swallowed by the compounding beast

- First, pay off your balance in full each month. Credit cards have this thing called a grace period, where your purchases won’t accrue interest if you pay the statement balance in full. Easy peasy, right?

- Or, you can play the game strategically and take advantage of introductory 0% APR offers. Some credit cards will treat you to a 0% APR during a limited time period. It’s like getting a free pass to avoid accruing interest on your purchases. Just make sure you have a plan to pay off that balance before the promotional period ends, or it’s back to the compounding madness.

- And hey, if you’re drowning in credit card debt, consider transferring your balance to a balance transfer credit card. These bad boys offer a promotional 0% APR on transferred balances, giving you some breathing room to pay off your debt without the compounding gloom. Just be sure to read the fine print, because compounding may still rear its ugly head for new purchases.

- Oh, and one more thing – improving your credit score can save you when the compounding beasts come knocking. A better credit score can get you lower interest rates, cutting those annoying interest charges.

- Check out FreedomPath’s DIY credit restoration software to tackle your credit score and crush those compounding monsters.

In conclusion, compounding interest and credit card debt may seem daunting, but armed with the right knowledge and strategies, you can slay those beasts and free yourself from the clutches of unnecessary interest charges. So go forth, my friend, and conquer the world of compounding interest!